On-Chain Trading Data Gaps: Risks for Crypto Market Oversight

This article was originally published in Financial Columnist. You can find the original post on their website here."

This article is adapted from a presentation delivered at the Federal Reserve Bank of New York in April, 2025, where Ethan Chan (CEO, Allium) shared insights on the state of on-chain trading and its implications for consumer protection and market oversight.

Authors: Ethan Chan, William Lai, Carlos Cortes Gomez

-

As of mid-2025, crypto exchange trading volumes have reached unprecedented levels, spiking above $1.8 trillion in a single month (The Block). Despite millions of new retail traders coming on-chain every month, these participants face two systemic disadvantages: 1) Incomplete market data and 2) Inconsistent trade execution quality.

These inefficiencies are not just an inconvenience for retail traders. They raise risks for the broader market, exposing consumers to predatory practices and undermining trust in digital asset markets. For regulators and institutions, these gaps create blind spots that complicate oversight, risk management, and consumer protection.

This article outlines what Allium’s analysis uncovers about today’s crypto trading environment, how our data methodology establishes trust in those findings, and why lessons from traditional finance are directly relevant for regulatory oversight of blockchain markets.

More New Consumers Jumping into Crypto Trading

According to Allium’s data, on-chain trading volumes spiked to $1 trillion in January 2025. This period marked a memecoin trading frenzy, particularly driven by $TRUMP – a memecoin US President Donald Trump launched on the Solana blockchain platform. Volumes declined following January, but have risen steadily since March.

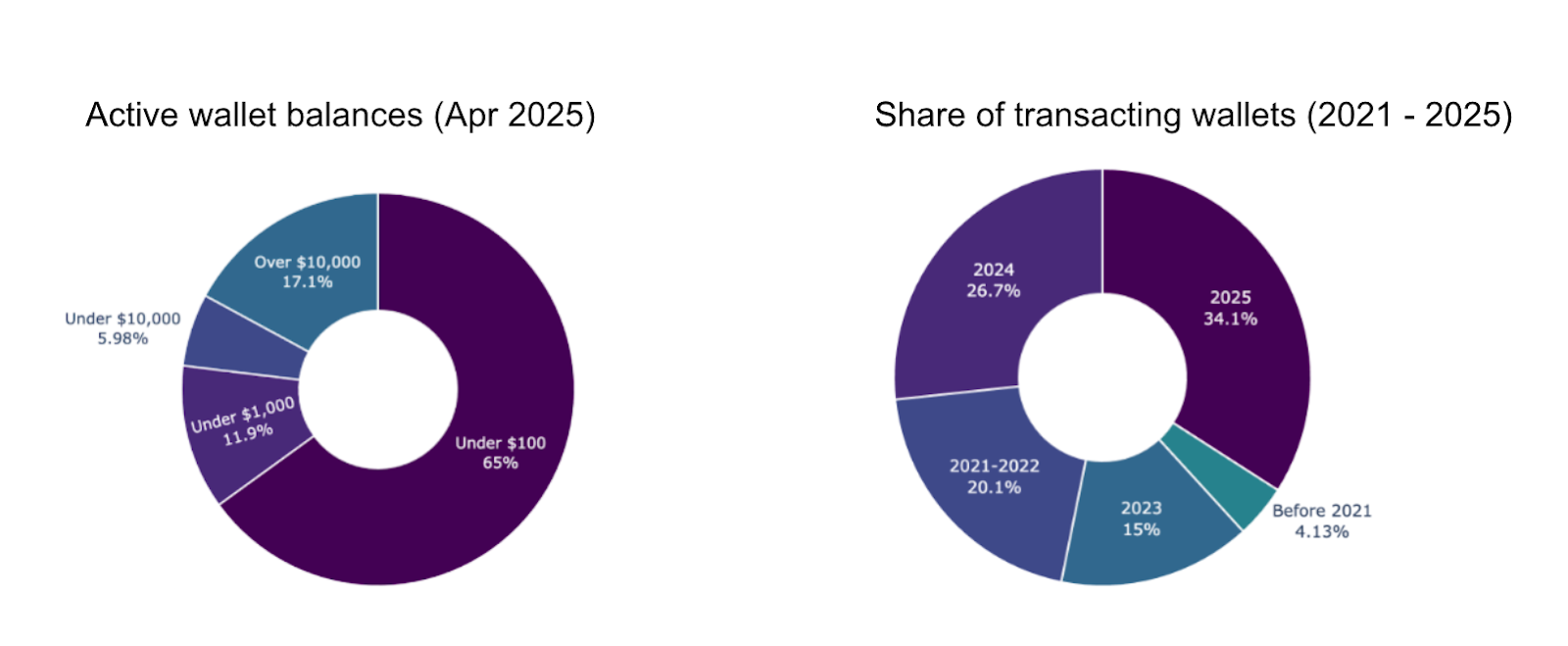

Most of the traders involved appeared to be new retail participants – 65% of active wallets maintain balances below $100, and 34% of transaction-executing wallets were created during 2025.

Allium analyzed historical and real-time on-chain data across more than 260 DEX protocols on 100+ blockchains, then built a dataset of liquidity pairs traded on at least three protocols across one month. This filtering ensured statistically robust point estimates instead of one-off outliers. By contrasting relatively more “stable”, high-liquidity pairs such as USDC:WETH and AERO with volatile memecoin pairs like Bananas, and by measuring execution-price variance across routers and aggregators, we quantified the two key disadvantages retail traders face with rigorous, reproducible evidence.

Incomplete market data exposes retail traders to price volatility

Most retail traders lack access to consolidated, high-quality market data. In practice, most consumers rely on public dashboards or exchange-provided APIs, which often omit large portions of trading activity or present it with significant time lags. Unlike institutions, they lack access to high-quality, consolidated feeds that aggregate across hundreds of fragmented liquidity sources.

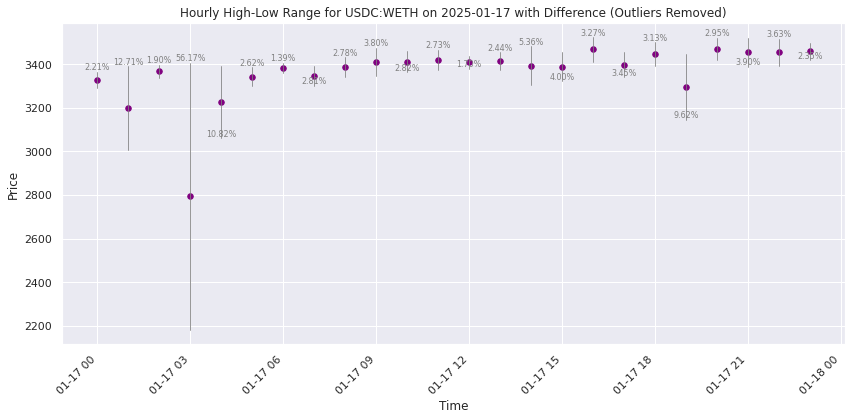

Large-cap tokens like WETH trade at 2–3% spreads under normal conditions, with spikes of 10–55% during peak volatility.

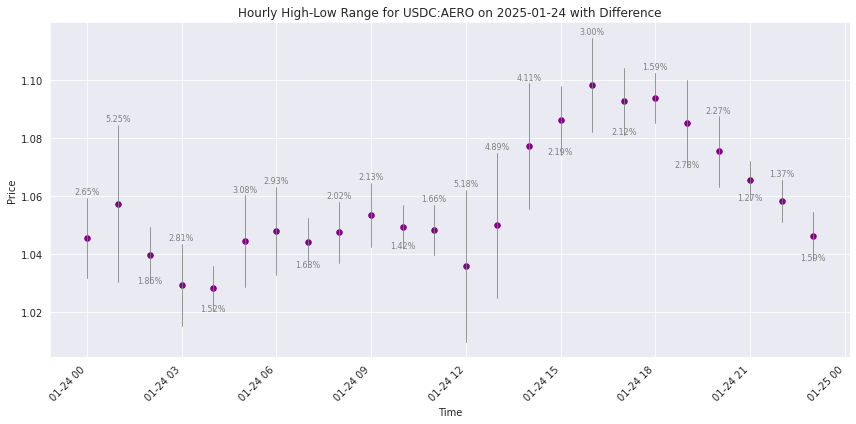

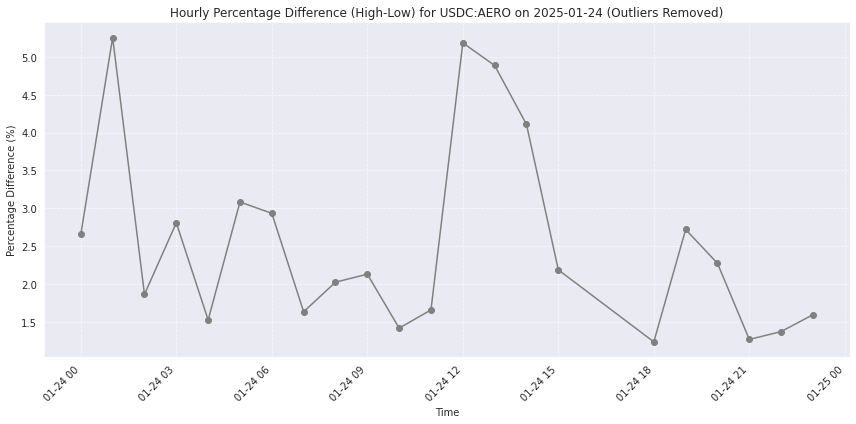

Smaller cap tokens like AERO trade at even higher spreads, often seeing a 3-5% divergence.

Allium's data showed an inverse correlation between token market cap and price divergence, creating information asymmetry for traders of smaller or newer assets.

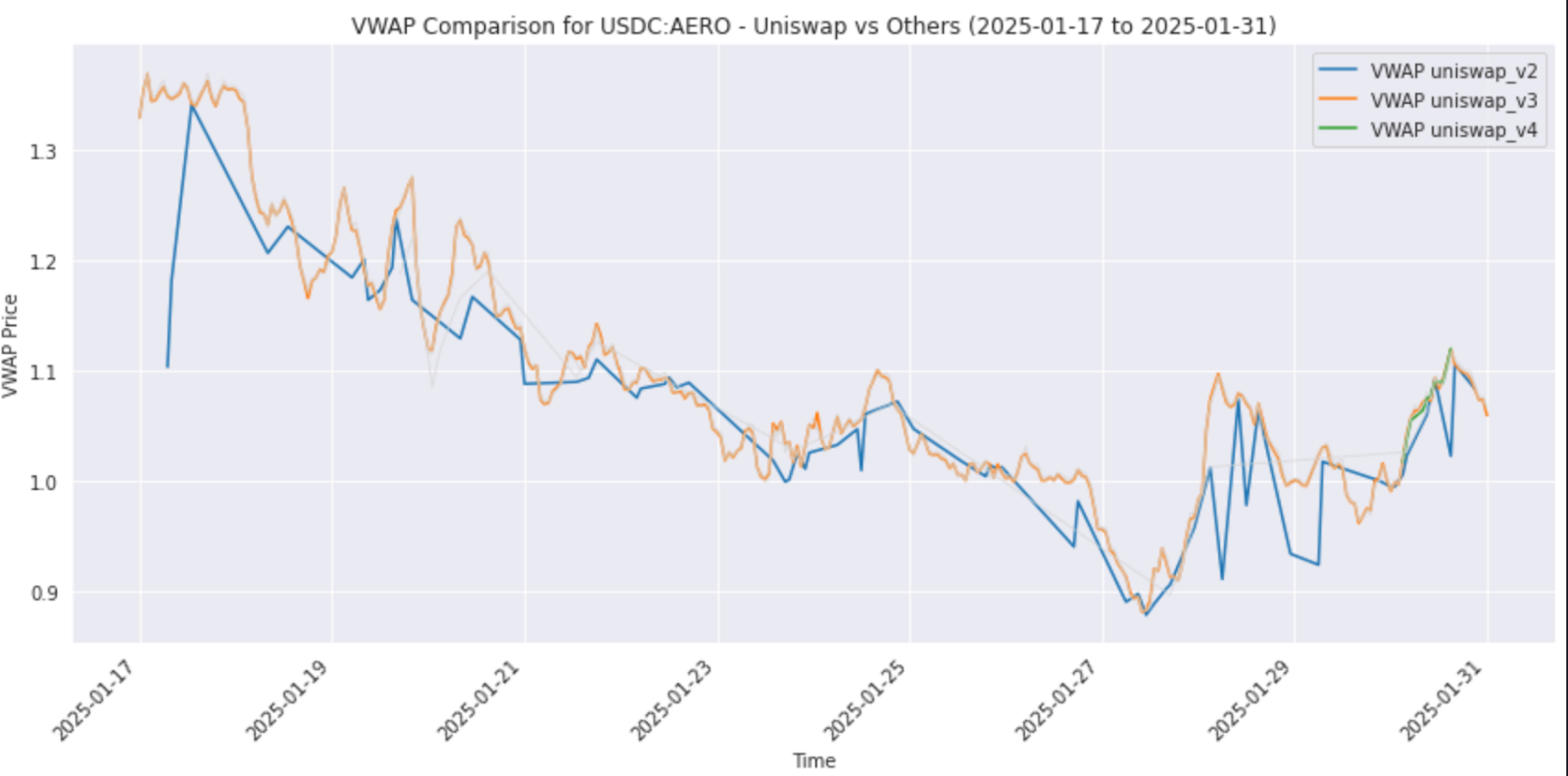

Pricing for the same token fluctuates across different DEXes: Allium found that various versions of the Uniswap protocol (v2, v3, v4) displayed price variations of 1-10% for identical USDC:AERO trading pairs.

For regulators, this fragmentation means that a single retail trade may execute at a materially worse price depending on the venue chosen, often without the consumer knowing. Without consolidated data, the market cannot be effectively monitored for fairness, stability, or abuse.

Inconsistent Execution Quality

Trade execution adds a second layer of consumer disadvantage, as even liquidity aggregation protocols designed to optimize trade routing vary widely in quality.

Liquidity aggregation protocols (e.g. 1inch, Matcha) scan across many DEXs and DeFi platforms to find and pool the most competitive prices, routing a trade through optimal paths, minimizing slippage and fees. While these protocols combat price divergence in theory, this often crumbles in practice for several reasons, as shown via Allium data.

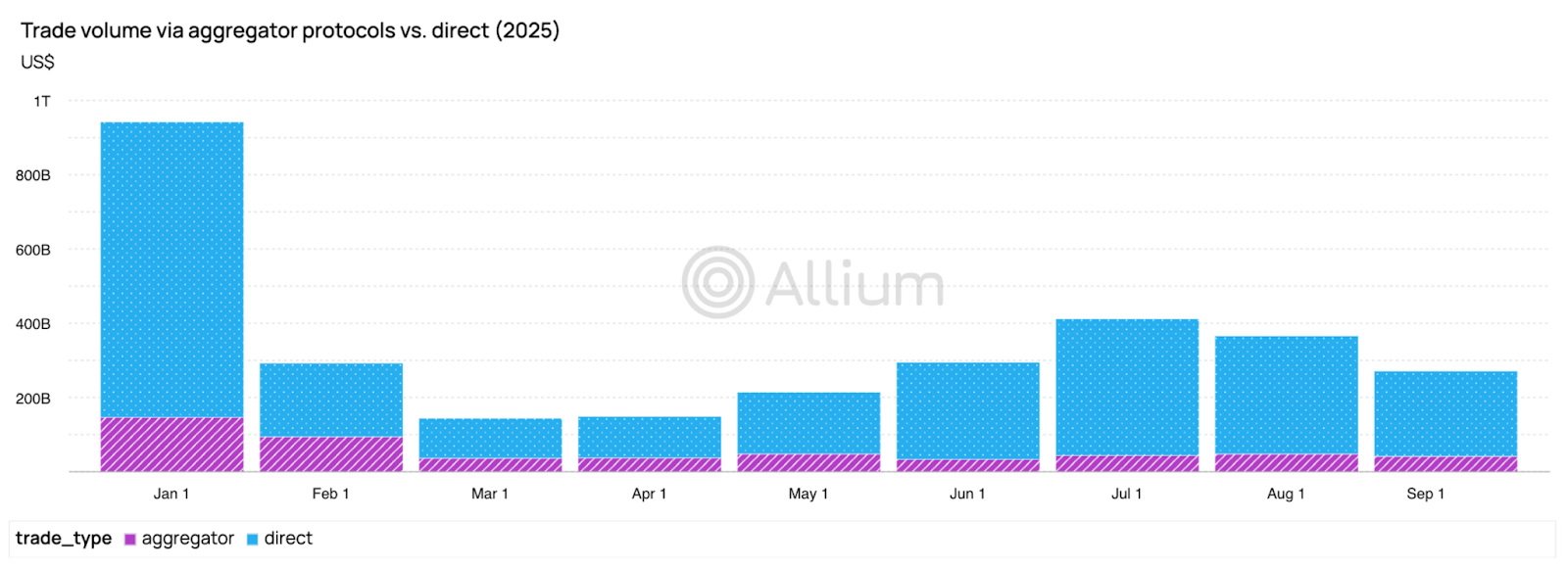

Aggregator protocols are rarely used in practice: Only ~17% of Solana DEX trade volume is routed through aggregators.

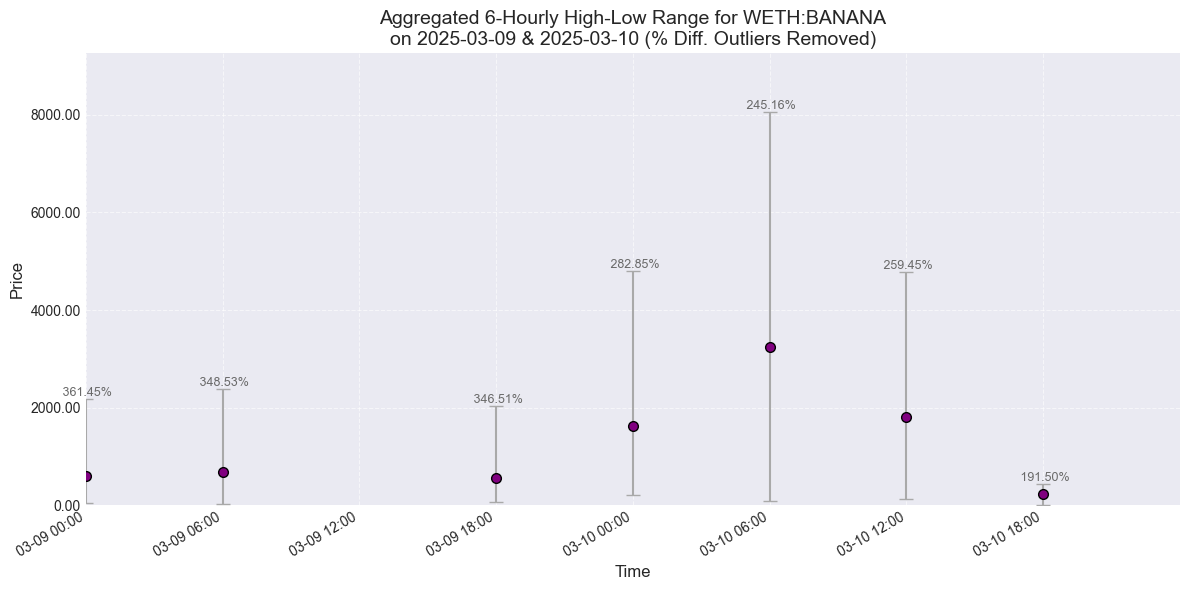

When used, aggregators still diverge in execution quality: Allium found that for small-cap tokens and memecoins, even liquidity aggregators diverge in execution performance. In this case, a small-cap memecoin like BANANA saw a price spread of 200-350%.

BANANA price spread on March 10, 2025

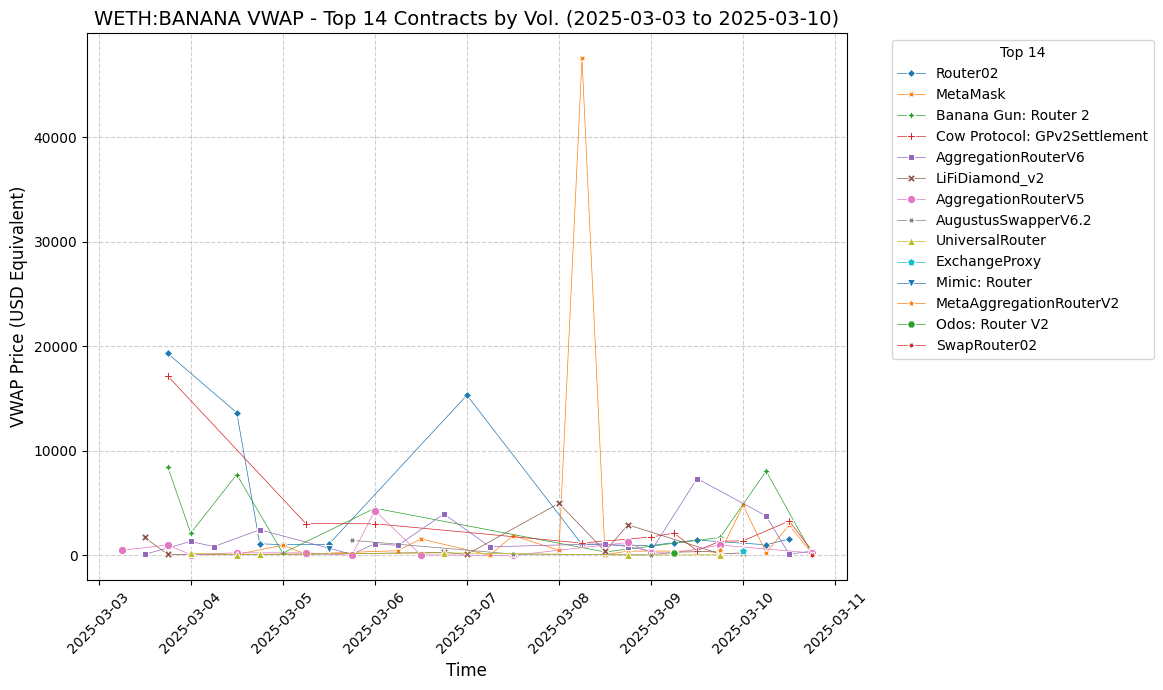

Aggregator execution quality varies by token, timeframe and market conditions: For the same token (BANANA memecoin), the VWAP price diverged significantly within the span of a week, across more than 10 different aggregators.

In practice, this means that two consumers executing the same trade at the same time can experience dramatically different outcomes. 21% of Solana DEX trades YTD saw 3% or more slippage - with those high-slippage trading wallets being more likely to be recently onboarded.

Worse, consumer-facing trading interfaces often obscure slippage or execution details in the name of simplicity. This leaves traders—especially newcomers more likely to see high slippage—exposed to MEV bots and other automated systems that exploit retail transactions via tactics like front-running and sandwich attacks (front-running and back-running to profit from slippage). Consumers are “bringing a knife to a bot fight”.

What crypto can learn from institutional finance to protect consumers

These issues are not unique to crypto. Traditional finance solved similar problems decades ago with two key solutions:

- Consolidated Market Data (U.S., SEC, 1975): After a 1971 SEC study showed retail investors were disadvantaged by fragmented quotes, Congress amended the Securities Acts (1975), requiring Securities Information Processors (SIPs) to aggregate quotes and trades. This created the National Best Bid and Offer (NBBO)—a single benchmark visible to all investors.

- Best Execution (U.S., Reg NMS 2005; FINRA): The SEC’s Reg NMS Rule 611 banned “trade-throughs,” requiring routing to NBBO prices. FINRA Rule 5310 imposed a duty of best execution, considering price, speed, and likelihood of fill. These rules set outcome benchmarks regulators could measure.

Implication for on-chain markets: Similar tools—consolidated data, enforceable routing standards, and transparent execution reports—could shrink retail disadvantages. These improvements would particularly benefit newer market participants, who face the steepest disadvantages today. By establishing industry-wide data transparency, markets can better serve all participants—regardless of experience level or resources.